Florida Hurricane & Tropical Storm Preparedness Guide

What Every Gulf Coast Homeowner Should Know Before, During & After Storm Season

If you're new to Florida, hurricane season can feel overwhelming.

Every year thousands of families move to Pensacola, Navarre, Gulf Breeze, Pace, Milton, Cantonment, Crestview, Niceville, Destin and the surrounding Gulf Coast from states that rarely experience hurricanes.

Many don't realize that standard homeowners insurance doesn't cover everything a hurricane can damage.

This guide explains:

- How hurricanes affect insurance

- What coverages you should consider

- How to prepare your home

- What to do before and after a storm

- Frequently misunderstood insurance terms

- Helpful emergency resources

Whether you've lived here for thirty years or thirty days, preparation is one of the best ways to protect your family.

Understanding Hurricane Season in Florida

Living along Florida's Gulf Coast means enjoying beautiful beaches, boating, and year-round outdoor activities—but it also means being prepared for hurricane season. Understanding how tropical systems develop and what the different storm categories mean can help you make informed decisions to protect your family, your home, and your finances.

Hurricane Season: June 1 – November 30

The official Atlantic hurricane season runs from June 1 through November 30 each year. While tropical systems can occasionally develop outside these dates, the vast majority of storms occur during this six-month period.

Residents of Pensacola, Navarre, Gulf Breeze, Milton, Pace, Crestview, Destin, Panama City, and surrounding Gulf Coast communities should review their insurance coverage and emergency plans well before the season begins.

Peak Hurricane Activity: August Through October

Although storms can develop at any time during hurricane season, August, September, and October are typically the busiest months. During this period, ocean temperatures are at their warmest, providing the fuel tropical systems need to strengthen quickly.

Because storms can intensify rapidly, it's important not to wait until a hurricane is approaching to prepare your home or review your insurance coverage.

Understanding Tropical Weather Systems

Not every tropical system becomes a hurricane. Here's what the different classifications mean:

Tropical Depression (Winds up to 38 mph)

A tropical depression is the earliest stage of a developing tropical system. It has a defined circulation but sustained winds remain below 39 mph. While these systems may seem minor, they can still produce heavy rainfall, localized flooding, and isolated tornadoes.

Tropical Storm (39–73 mph)

When sustained winds reach 39 to 73 mph, the system is classified as a tropical storm and receives an official name. Tropical storms can cause:

- Heavy rainfall

- Flash flooding

- Coastal flooding

- Downed trees

- Power outages

- Minor to moderate property damage

Preparation should begin as soon as a tropical storm is forecast to impact your area.

Hurricane (74+ mph)

Once sustained winds reach 74 mph or greater, the storm becomes a hurricane. Hurricanes are categorized using the Saffir-Simpson Hurricane Wind Scale, which measures expected wind damage.

| Category | Sustained Winds | Potential Damage |

|---|---|---|

| Category 1 | 74–95 mph | Damage to roofs, siding, trees, and power lines. Power outages may last several days. |

| Category 2 | 96–110 mph | Significant roof and siding damage, widespread tree damage, longer power outages, and blocked roads. |

| Category 3 (Major Hurricane) | 111–129 mph | Major structural damage to homes, extensive tree loss, widespread utility outages, and dangerous storm surge. |

| Category 4 | 130–156 mph | Severe structural damage, many homes losing portions of their roofs or walls, prolonged power outages, and life-threatening storm surge. |

| Category 5 | 157+ mph | Catastrophic damage with many homes destroyed, extended utility outages, and severe flooding and storm surge impacts. |

Important: A hurricane's category is based only on wind speed. Even lower-category storms can produce devastating flooding, tornadoes, and storm surge. Never focus solely on the category number when deciding whether to prepare or evacuate.

Stay Informed Throughout Hurricane Season

Weather forecasts can change quickly, especially during peak hurricane season. We recommend monitoring official forecasts regularly and following guidance from local emergency management officials.

For the latest forecasts, storm tracking maps, watches, warnings, and preparedness information, visit the National Hurricane Center (NOAA).

Knowing what to expect before a storm develops is one of the most effective ways to protect your family and your property. The earlier you prepare, the more options you'll have if severe weather threatens the Gulf Coast.

What Does Homeowners Insurance Cover During a Hurricane?

Wind Damage

Typically covered.

Examples:

- Roof damage

- Broken windows

- Fallen trees

- Siding damage

Water Damage

Water damage can be one of the most confusing parts of hurricane insurance because not all water damage is covered the same way.

Generally:

- Rain that enters your home because wind damaged your roof, siding, or windows is typically covered under a standard homeowners insurance policy.

- Floodwater that rises from the ground outside your home, such as storm surge, overflowing rivers, or heavy rainfall that causes flooding, is not covered by standard homeowners insurance and requires a separate flood insurance policy.

Understanding the difference before a storm arrives can help prevent unexpected surprises when it's time to file a claim.

Example: If hurricane winds tear shingles off your roof and rain enters through the damaged opening, that is generally considered wind-related damage. If several inches of water enter your home because streets or storm surge flood your property, that is considered flood damage and typically requires flood insurance.

Flood Insurance: One of the Most Important Coverages for Florida Homeowners

One of the biggest misconceptions we hear from new Florida residents is, "My homeowners insurance covers flood damage."

Unfortunately, it usually doesn't.

Standard homeowners insurance policies typically cover wind damage, hail, fire, lightning, and other covered perils, but they do not cover damage caused by rising water. If floodwater enters your home from storm surge, overflowing rivers, heavy rainfall, or other natural flooding events, those damages are generally excluded from a standard homeowners policy.

What Is Flood Insurance?

Flood insurance is a separate insurance policy specifically designed to protect your home and belongings from flood damage caused by rising water. Depending on the policy you choose, it can help pay to repair your home's structure, replace damaged personal property, and assist with recovery after a flood.

Many flood insurance policies are available through the National Flood Insurance Program (NFIP) as well as private insurance carriers, giving homeowners multiple coverage options.

Do I Need Flood Insurance?

Even if your home is not located in a high-risk flood zone, it's worth evaluating your flood risk.

In fact, a significant percentage of flood insurance claims each year come from properties outside of designated high-risk flood zones. Heavy rainfall, tropical storms, hurricanes, drainage issues, and storm surge can all cause flooding in areas that have never flooded before.

If you live anywhere along Florida's Gulf Coast—including Pensacola, Navarre, Gulf Breeze, Milton, Pace, Cantonment, Crestview, Niceville, Destin, or surrounding communities—we recommend discussing flood insurance with your insurance agent to determine whether it's appropriate for your property.

Don't Wait Until a Storm Is Approaching

Flood insurance is designed to be purchased before a storm is on the way. Most policies include a waiting period before coverage becomes effective, which means you generally cannot wait until a hurricane has been named or is approaching the Gulf Coast to purchase protection.

The best time to review your flood insurance options is well before hurricane season begins.

Good to know: Wind damage and flood damage are treated differently by insurance companies. A hurricane can cause both at the same property, which is why understanding your coverages before a storm arrives is so important.

Wind vs. Flood

🟢 Typically Covered by Homeowners Insurance

- Wind damage to your roof

- Fallen trees

- Broken windows from wind

- Wind-driven rain entering through storm-created openings

🔵 Requires Flood Insurance

- Storm surge

- Rising water entering your home

- Overflowing rivers or creeks

- Streets or yards flooding into your home

Understanding Named Storm Deductibles

Many Florida homeowners are surprised to learn that their hurricane deductible may be much higher than their standard homeowners deductible.

For most claims, you may have a fixed deductible such as $2,500. However, if your policy includes a Named Storm or Hurricane Deductible, your deductible may instead be a percentage of your home's insured value (Coverage A).

Common Named Storm Deductibles

| Coverage A (Home Value) | 2% Deductible | 5% Deductible | 10% Deductible |

|---|---|---|---|

| $250,000 | $5,000 | $12,500 | $25,000 |

| $350,000 | $7,000 | $17,500 | $35,000 |

| $400,000 | $8,000 | $20,000 | $40,000 |

| $500,000 | $10,000 | $25,000 | $50,000 |

| $750,000 | $15,000 | $37,500 | $75,000 |

When Does a Named Storm Deductible Apply?

A named storm deductible typically applies only when damage is caused by an officially named tropical storm or hurricane, as defined by your insurance company and policy.

For other covered claims—such as a kitchen fire, burst pipe, or theft—your standard homeowners deductible usually applies instead.

Why It Matters

Knowing your deductible before hurricane season helps you plan financially and avoid surprises after a storm. If you're unsure whether your policy has a named storm deductible—or how much it is—our team at Gulf Coast Insurance can review your policy and explain your coverage in plain English.

Coverages Worth Considering Before Hurricane Season

Nice table:

| Coverage | Why it Matters |

|---|---|

| Flood Insurance | Rising water isn't covered under homeowners |

| Sewer Backup | Heavy rain can overwhelm systems |

| Service Line Coverage | Underground utility lines |

| Equipment Breakdown | HVAC, electrical systems, appliances |

| Extended Replacement Cost | Inflation after storms raises rebuilding costs |

| Ordinance or Law Coverage | Building code updates |

The Equipment Breakdown and Service Line section is a great opportunity to summarize the concepts from the article the user shared and explain how they differ from service contracts in simple language rather than duplicating it.

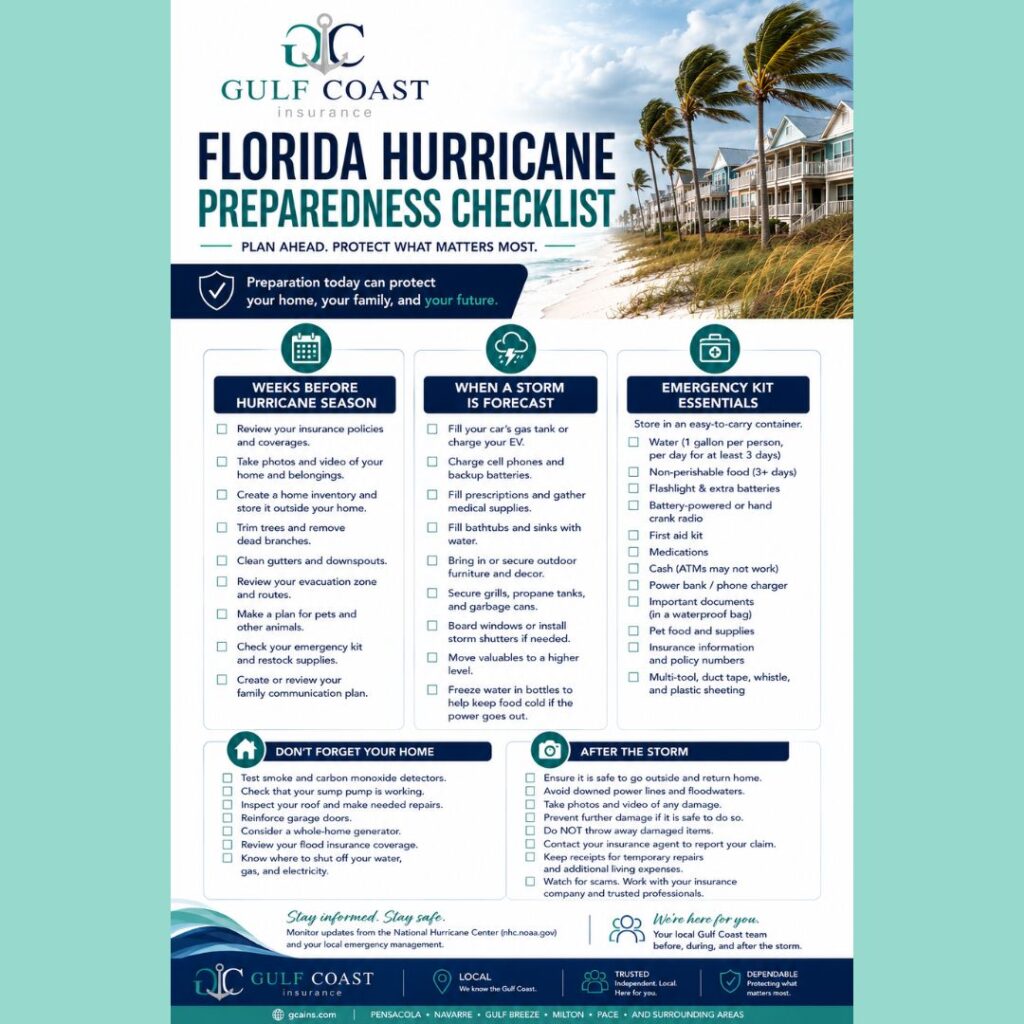

Hurricane Preparation Checklist

Weeks Before Hurricane Season

- Review insurance

- Take home photos

- Inventory valuables

- Trim trees

- Clean gutters

- Review evacuation zones

- Prepare pet plan

When A Storm Is Forecast

- Fuel vehicles

- Charge electronics

- Fill prescriptions

- Fill bathtubs

- Bring patio furniture inside

- Secure grills

- Board windows if needed

- Move valuables

- Freeze water bottles

- Charge battery packs

Emergency Kit

- Water

- Food

- Medicine

- Flashlights

- Battery radio

- Power banks

- Cash

- Pet food

- Important documents

- Insurance information

What To Do After the Storm

- Photograph damage.

- Prevent additional damage if safe.

- Do NOT throw damaged items away.

- Contact insurance.

- Keep receipts.

- Watch for scams.

Insurance Claim Tips

- Take hundreds of pictures.

- Keep damaged materials.

- Save hotel receipts.

- Document temporary repairs.

- Don't sign anything immediately from storm chasers.

Helpful Resources

- National Hurricane Center (NOAA)

- FEMA

- Florida Division of Emergency Management

- Escambia County Emergency Management

- Santa Rosa County Emergency Management

- Okaloosa County Emergency Management

Local Areas We Serve

- Perdido Key

- Pensacola

- Pensacola Beach

- Gulf Breeze

- Orange Beach, AL

- Gulf Shores, AL

- Innerarity Point

- Lillian, AL

- Warrington

- Myrtle Grove

- Bellview

- Cantonment

- Crestview

- Navarre

- Milton

- Pace

- Fort Walton Beach

- Mary Esther

- Shalimar

- Niceville

- Destin

- Panama City

Have Questions About Your Hurricane Coverage?

Storm preparation starts long before a tropical system appears on the radar. Whether you're buying your first home in Florida or have lived on the Gulf Coast for years, reviewing your insurance before hurricane season can help you avoid costly surprises.

Our team at Gulf Coast Insurance can review your current policies, explain deductibles and exclusions, and help you determine whether coverages like flood insurance, equipment breakdown, service line protection, or increased replacement cost may be appropriate for your needs.

Schedule a free insurance review before the next storm arrives.